Sales and use tax exemptions can be a complex issue for ecommerce retailers to understand, but it’s critical that they do. Without proper documentation, exemptions can fall apart and retailers can then find themselves in the midst of a costly audit. The problem is that all states have different laws and codes defining when and where these exemptions apply. Retailers may think that there is “one certificate to rule them all” but, in fact, the subtleties of state-to-state legislation and guidelines can make those certificates invalid or lead to incomplete filing of exemption certificates. Centralization documentation for all states does not exist yet, but two organizations are making headway toward that goal.

The Forms for Sales and Use Tax Exemptions Across Multiple States

First off, there are two forms by which retailers can obtain sales and use tax exemptions in certain states. They were each designed by a different group with a mission to create more level tax standards. They are:

1. Streamlined Sales Tax Agreement Exemption Certificate

This exemption certificate is a result of the efforts of the Streamlined Sales and Use Tax Governing Board, a collaboration of 44 states and the District of Columbia to unify sales and use tax laws through the Streamlined Sales and Use Tax Agreement (SSUTA). Retailers need to know the following:

- Many states have made compliance changes in recent months so if retailers are familiar with this form, they need to check those changes.

- 44 states and the District of Columbia are covered but this does not cover all states. In addition, only 23 states are full members, meaning they employ the SSUTA through laws, rules, regulations and policies. Tennessee is listed as an associate member, meaning it is compliant with most of the agreement but not necessarily each provision.

- Additional forms may be required to prove exemption status within the state.

- The form itself reads, “Not all states allow all exemptions listed on this form.” Retailers should keep in mind that if they are not eligible for the exemption and claim it, they would still be accountable for tax, interest, and possible civil or criminal penalties where it is not covered.

While this is a good beginning, fully relying on this certificate will not cover all states’ exemption requirements or regulations. However, there are some benefits, such as ease of adding the exemption for member states and the ability to use sales tax administration software, which may be eligible for subsidization. This is a good step towards centralizing the exemption process.

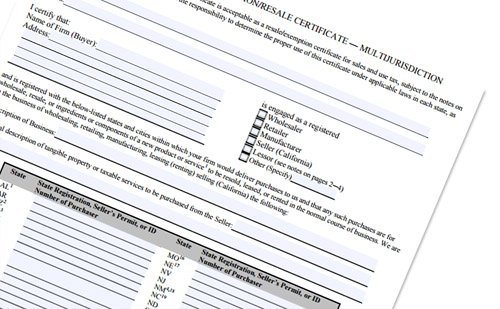

2. Uniform Sales and Use Tax Certificate – Multijurisdiction Form

The Multistate Tax Commission (MTC) is an agency working to “administer, equitably and efficiently, tax laws that apply to multistate and multinational enterprises.” Again, there are member states that work with this agreement. The Uniform Sales and Use Tax Certificate, sometimes referred to as the MJC (Multijurisdiction Certificate), is another form for registering exemptions with participating states. To use this form, retailers need to know the following:

- There are only 38 states that participate in the commission. Additionally, there are different classes of membership that involve different levels of involvement with the commission. Only 16 members as of this writing participate with the Multistate Tax Compact enacted into their state law.

- Retailers may need a reseller ID – or not. This varies from state to state and must be properly filed when required.

- This form requires each state’s proper identification, which may be called different things by the state. Filers need to know this information for the states they are applying for.

- The MTC itself writes on the form that they “cannot guarantee that any state will accept this certificate.” Retailers must pay close attention to the proper filing of this form.

It’s clear that while the MTC has numerous foundational plans both in place and in review to create an easier sales and use system, including a Nexus and Audit program, more work needs to be done before this system can replace state-by-state exemptions.

Again, there are similar benefits, but neither document is a substitute for knowing the sales and use tax exemption regulations in the state that a retailer or drop shipper is operating in or has a nexus in.

Best Practices for Filing These Exemptions

Hopefully, the Streamlined Sales Tax Governing Board and the Multistate Tax Commission can continue to work closely with states to move the processing of sales and use tax exemptions in a more efficient direction, but more work remains to be done. For now, ecommerce retailers should take the following best practices to protect themselves, whether or not they choose to use these forms:

- Both forms require that filers comply with each state’s rules for exemptions and when and where they apply. It’s critical to understand these regulations in any state that the retailer operates in before filing for exemption.

- That means retailers also need to understand how each state defines nexus and where the retailer has such a presence.

- When used, these forms must be filled out completely and accurately, and that documentation should be approved before any sales and use exemptions are done. In other words, retailers must make sure their exemption is in place before waiving sales or use tax.

- Incorporate certified sales tax administration software from a certified service provider to keep track of exemptions, filings and changes.

- Know when filing the forms allows for state-subsidized costs for the software.

- Ecommerce retailers can learn more about registering for the Streamlined Sales Tax Agreement at the Streamlined Sales Tax Project. At that site, they also provide links to additional tax registration requirements by state.

- You can also view the Uniform Sales & Use Tax Certificate online as well.

The MTC and SSUTA are taking helpful first steps towards centralizing state-by-state sales and use tax laws and regulations and can be useful for online retailers who employ best practices and are fully aware of state exemption regulations that affect them.